Comparison of Crisis Loans in Hungary – Which product is worth applying for?

In the following article, we summarize the crisis loans available within the state’s package of measures, showcase their most important qualities and unfold which solution is the most ideal for certain companies.

In the past weeks, many SMEs have faced management issues due to the ongoing COVID-19 crisis. The government’s response to the increased economic difficulties was a financial package, to provide the necessary resources for Hungarian companies in need. In most cases, the coronavirus has brought an unfavourable change for businesses, but it is certainly not impossible for them to survive during these times – a well-chosen loan can address the financial needs of the company. The aim of the government’s measures is to support domestic businesses in not only surviving this period but also to become successful participants in relaunching the economy.

The new loan schemes help small businesses in facing difficulties with low, mostly fixed annual interest rates. With its wide range of credit objectives, it allows SMEs to overcome their financial obstacles, ranging from liquidity shortages to executing major investments. Financial institutions aim to simplify the application process while ensuring favourable conditions, thus speeding up SME’s access to liquidity.

LOAN PRODUCTS CURRENTLY AVAILABLE AT HITELPONT:

MFB Business Financing Investment Loan

MFB Business Financing Working Capital Loan

What kinds of crisis loans are available on the market?

As several loan schemes have appeared in the recent months, we found it helpful to have a brief overview on the products, their most important conditions, their benefits, and what kinds of enterprises they are recommended for.

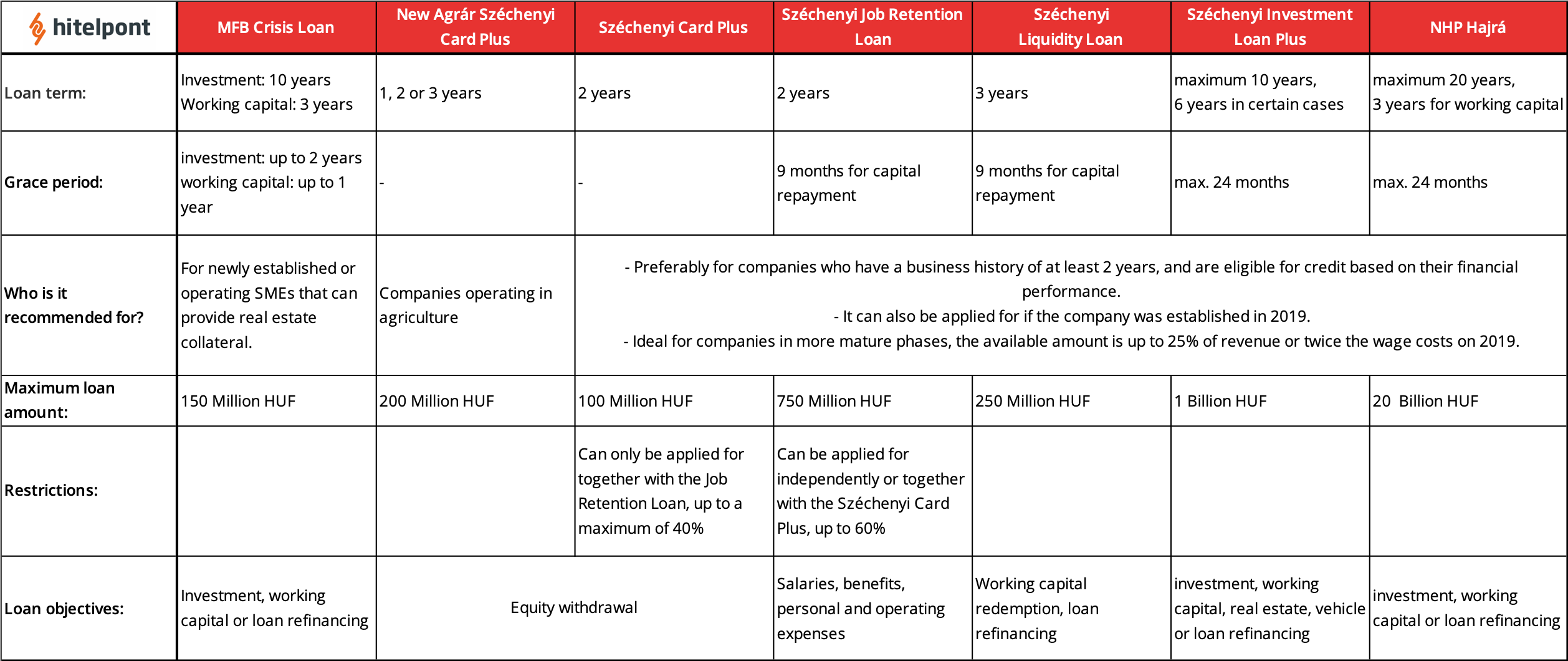

A general comparison of the new loans part of the government’s financing package

The NHP Hajrá funding scheme might provide a stable financial background for SMEs, it is available through commercial banks and can be used for general investment purposes, working capital financing or loan refinancing. The MFB Crisis Loan was created in accordance with the conditions of NHP Hajrá, it is rather ideal for companies whose loan application was denied by commercial banks for any reason, or do not meet the requirements proportional to revenue and personnel expenditures. The MFB Crisis Loan is also available for start-ups or newer companies, with a wide range of credit objectives and favourable interest rates.

The Széchenyi Card Program’s loans also play an important role, these schemes are provided by KAVOSZ. The Agrár Széchenyi Card Plus is a new product, it contributes to companies operating in the agriculture sector with special support by the state. This is a short-term loan that can be applied for a term of 1, 2 or 3 years, with an interest subsidy and a guarantee fee support provided by the government. The Széchenyi Card Plus is an overdraft, and it might be a great solution for companies with shortages in financing day-to-day expenditures.

It is good to know that by having an overdraft, the company is provided with a certain amount of credit, which they might use when needed. The budget is reviewed annually by the financial institution, and if a negative change is experienced in the economics, they can either reduce or even withdraw the credit line.

A wide range of products exists for the SMEs to choose from in times of the epidemic, the loans are available with low interest rates and on favourable terms. (Source: Dylan Gillis, Unsplash)

Another new product is the Széchenyi Job Retention Loan, it is a working capital loan that can be used for financing personnel expenditures, benefits, and other operational expenses (opex). It is important to note that while companies can apply for Széchenyi Job Retention Loan on its own, the Széchenyi Card Plus overdraft can only be applied for jointly with the Job Retention Loan. In this case, the ratio of the Card Plus product can be up to 40%, and 60% for the Job Retention Loan.

The Széchenyi Liquidity Loan is a working capital loan, which provides funding for transactions under 250 million forints, and the primary aim is to provide financing for short-term financial problems. The Széchenyi Investment Loan Plus can be used for investments, as well as financing working capital related to the investment, up to 20%.

Comparison of general conditions

Comparing the most important conditions can help us choose the loan scheme that fits our purposes and needs the most. In case of the Széchenyi loans, they are aiming to finance short-term funding gaps, the term is always less than 3 years. The exception is the Investment Loan Plus, where the objective also justifies a longer term, loans with investment objectives are mostly available for long-term, which can be a maximum of 10 years in this specific case. It is important to note that when talking about Széchenyi loans, the total loan amount is determined based on the financial performance of the previous years. For this, commercial banks usually assess the sales revenue and personnel expenditures among other financial indicators.

One of the main features of NHP Hajrá is that the term of investment loans can be extended to a maximum of 20 years. In the case of the MFB Crisis Loan, the term can take up to 10 years, whereas the maximum term for the working capital loan can be as of 3 years.

One of the biggest advantages of the Crisis Loan is that it can also be applied by start-ups or newly established SMEs, it is not necessary to provide a financial report from the previous years. At the same time – unlike other types of loans – it is also available for clients whose needs have been rejected by commercial banks, as real estate collateral is the primary security requirement. The loan amount can range from 1 million to 150 million HUF, and can be used for investment objectives, financing of current assets as well as refinancing an existing loan.

Comparison of the most important conditions of the new COVID-19 crisis loan products

There are significant differences when it comes to loan amounts. The NHP Hajrá loan can be used for realizing major investments, up to 20 billion HUF (as it shows, this product mostly serves larger companies). The MFB Crisis Loan provides capital for SMEs up until 150 million HUF.

Most of the available loans are recommended for companies that already have a longer business history and have financial statements for the previous years. As these loans rely heavily on the company’s financial performance, the loan amount and creditworthiness are being determined based on these indicators, therefore these products are recommended for more mature companies. (these products include: Széchenyi Card Plus, Széchenyi Workplace Retention Loan, Széchenyi Liquidity Loan, Széchenyi Investment Loan Plus, NHP Hajrá)

The new ASZK Plus provides favourable conditions for companies operating in agriculture, the loan supports companies with 100% state interest subsidy and guarantee fee subsidy, but an important condition is that for a loan amount under 25 million HUF, the company is expected to have at least one closed business year, and above 25 million HUF, at least 2 years are required.

Restrictions, expectations

As mentioned before, applying for loans is based on the company’s financial performance in most cases. Commercial banks usually determine the maximal amount as a certain percentage of their sales revenue, this way it is inevitable to have a financial statement for the previous year.

In general, in case of the Széchenyi products, this ratio is 25% of the sales revenue, and in case of the NHP Hajrá, the amount is usually 30-40%. A simple example of this is when a company’s revenue was 100 million HUF in 2019, the highest loan amount available is 25 million HUF, or 30-40 million HUF in case of the NHP Hajrá. The loan amount is determined differently when it comes to the MFB Crisis Loan, which is also offered by Hitelpont. Our products are available with real estate collateral, and mostly the market value of the property serves as a base for calculating the loan amount.

The loan application process at Hitelpont is quick and simple, SMEs can access funding in as little as 2 weeks. (Source: bruce mars, Unsplash)

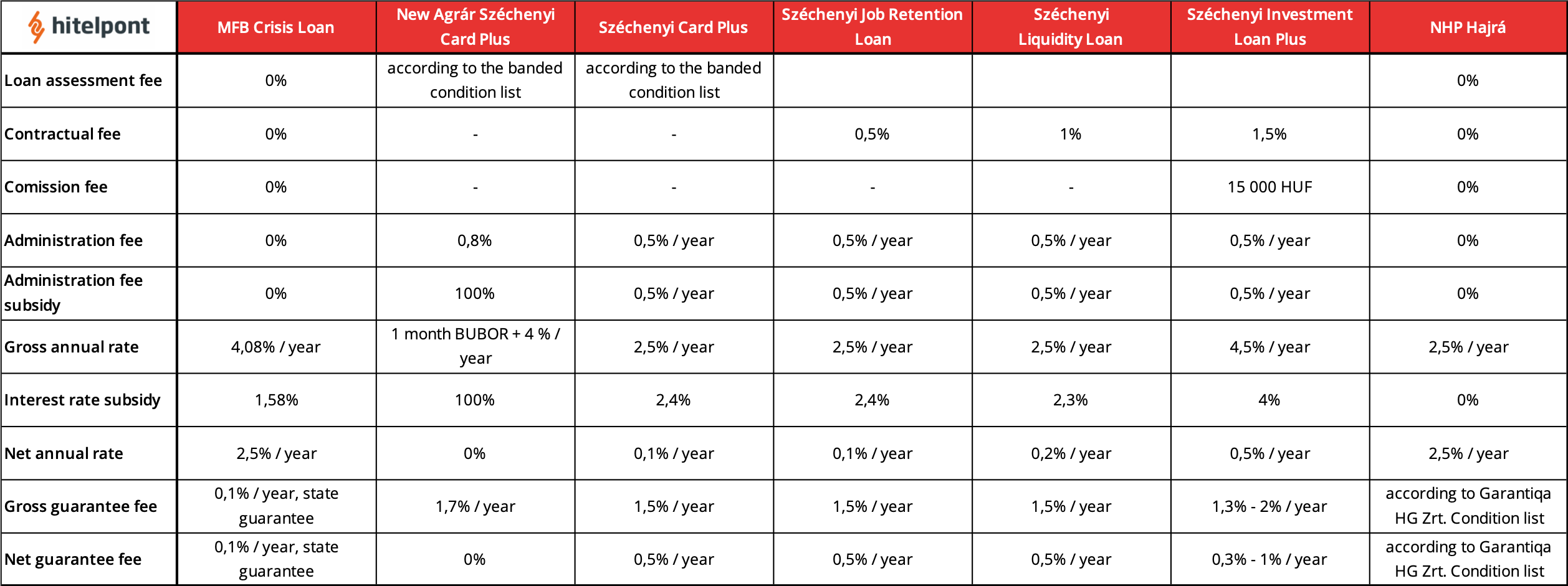

Costs – interests, fees, subsidies

The loans are available on very favourable terms, considering the crisis. The interest rate of NHP Hajrá and MFB Crisis Loan cannot be more than 2.5%, in case of the latter, the state guarantee fee is 0.1%. No other costs can be charged apart from these.

The Széchenyi Job Retention Loan and the Széchenyi Card Plus can also be applied for with an interest rate of 0,1%, in addition to a guarantee fee of 0.5%. The interest rate of the Széchenyi Liquidity Loan is 0.2%, another 0.5% is charged as a guarantee fee and an additional 1% contract fee.

A great advantage of the MFB Crisis Loan over the other products available on the market is that it can be used for multiple loan objectives, the application process is quick and simple, it can be applied for without considering the financial performance of the previous years and it provides financing under competitive conditions for those companies, who do not have access to funds at commercial banks.

In case you are interested in any of our loan schemes, you can obtain more information by clicking on the Our Products button. On the bottom of all the loan product pages, you can find the loan calculator, which can be used to calculate the expected repayment installments. The loan application process can be initiated online, it is also possible to request a callback from one of our colleagues. Should you have any other questions or be interested in a loan product available at Hitelpont, please call our customer service directly at +36-(70)-654-2486 or reach out to us at one of our Contact details.

RELATED ARTICLES:

2020.05.16. – Why financial enterprises can be good alternatives when our loan application gets rejected by commercial banks?